The following is a guest post from Ben Carlson at A Wealth of Common Sense. Ben writes about personal finance, investments, investor psychology and using your common sense to manage your money. You can follow him on Twitter (@awealthofcs).

If you missed part one of my series on rising interest rates, please read What Happens to Bonds When Interest Rates Rise.

Rising Interest Rates Affect on High Yield Investments

Rising interest rates are a hot topic in the ever changing investment landscape these days. Historically low rates have forced investors to prepare for the inevitable rate increase. And, this is especially true when you have high yield investments.

Investors searching for yield in an environment of low-interest rates have had a difficult time finding safe investments that also pay a decent income. Money markets, bonds, CDs and other interest bearing assets no longer provide enough income for investors that seek a consistent payout.

Outside of dividend stocks investors don’t have many options. This has led investors to look in places like preferred stocks, high yield bonds and REITs (real estate investment trusts) for income.

Chasing yield can be dangerous, but investors seeking income are left with few choices in a low rate world. Interest rates have little room to fall much further. Investors are now shifting their attention to how these high yielding investments will perform in a rising rate scenario.

Are Rising Rates the Real Problem?

It is definitely possible that we could have a shock to the system and interest rates could rise dramatically in the short-term. But, more than likely, we will see a slow and steady climb in rates. This will likely occur as central banks around the globe either start selling the bonds they have bought back to the market, or slow the rate of their future purchases.

It is possible that rates scream higher, but the most likely scenario is that rates slowly move higher over time. The diversified portfolios can be rolled over to take advantage of the new higher rates.

So while they will have some risk of price loss, the increasing yields will help offset some of those losses. Central banks will do their best to make sure rates don’t head higher in a short amount of time. Governments are borrowing short-term debt so it’s in their best interest to make sure it is a gradual process.

I think that investors are actually looking in the wrong place for the risk of losses in this case. Sure, if and when rates do eventually rise, high yield investments will run into some trouble.

But, if you are investing in preferred stocks, high yield bonds or REITs in the form of a diversified mutual fund or ETF your risk will be spread out and the losses will not be that severe with rising rates.

The bigger risk that investors are overlooking these new higher yielding investments is what happens when the risk-on trade reverses and markets turn cautious again.

Using History of High Yield Investments as a Guide

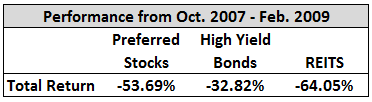

History is not a perfect predictor of the future but you can it as a framework for viewing current and future market decisions. Let’s see how preferred stocks, high yield bonds, and REITs performed in the most recent crisis. For each asset class, I will use a corresponding diversified ETF (PFF, JNK, and VNQ for preferreds, high yield, and REITs, respectively). Here are the total returns for each from October 2007 to February 2009:

This was a huge crash that also saw stocks drop over 50% in some markets. Many investors were looking for any source of liquidity that they could find since credit markets were basically frozen. These three assets were lumped in and it was a case of throwing the baby out with the bath water. hey have all since performed very well, although JNK and PFF have still not reached their 2007 peaks.

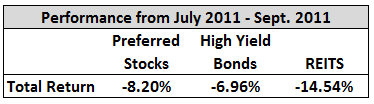

The point is not that you can expect losses of this magnitude if you invest in these assets, but just that they can sell off in a downturn. Let’s look at a more run-of-the-mill sell-off in risk assets that occurred in mid-2011 to see how they held up. From July to September of 2011 the European debt crisis caused stocks to sell off roughly 20%. Here’s how these higher yielding investments fared:

The performance was not nearly as bad as the losses in the 2007 to 2009 period but there were losses nonetheless. You can see that they all outperformed stocks (bond returns would look much better).

Conclusion

Since these securities are all hybrid investments that share both bond and stock characteristics you can expect them to perform somewhere in between those two main asset classes.

The main takeaway here is that you do have to worry about rising rates when investing in high yield investments, just not as much as you may think. The much bigger risk is what can happen to these investments when markets sell off as they have been periodically shown to do in the past.

As always, do your homework and think about the risks involved with your investments before you think about the returns.

Subscribe

If you enjoy receiving the Dividend Ninja in your mailbox, don’t forget to also subscribe to the Dividend Ninja Newsletter. Thanks for reading!

I concur that high yielding dividend stocks can be dangerous and chasing them can wipe out your portfolio as quickly as just trading stocks or day trading them.

I’ve been there myself. in the past I had a few high yielding stocks, which over time continued cutting the dividend (so everything I ever made in dividends was lost on principal) or in case of CEF the NAV was falling and the result was the same.

Over time I learned to take 3 – 4% yield now, which over period of 20 years can grow to 20% yield on original cost.

Hi Martin,

I think Ben is specifically referring to High Yield Bonds via the JNK ETF, REITs, and Preferred Shares. These three assets have generally higher (or much higher) yields than regular bonds.

REITs have higher yields simply becuase they do not pay corporate tax, and pass the taxation onto unit-holders (in Canada). Therefore there is a higher yield to offset the taxation. Plus they are required under law to distribute a higher percentage of their earnings back to unit holders than corporations (typical dividend paying stocks) are.

For Preferred Shares (specifically perpetuals) the rate is higher as the rate is tied into the longer end of the yield curve (10 year bonds or longer). Junk bonds speak for themselves – the rate is higher because of the risk.

But your absolutely right about the dangers of high yield stocks. Check out these two posts, for the specifics on those:

http://www.dividendninja.com/the-lure-and-dangers-of-high-yield-stocks-1/

http://www.dividendninja.com/the-lure-and-dangers-of-high-yield-stocks-2/

Cheers

Avrom

Avrom,

I am aware that Ben was primarily talking about bonds (and since I do no like bonds) I used this same logic on stocks. As you mentioned REITs are different creatures, but they can burn you very well too. The most recent example would be Armour Residential.

Martin, I get your take on bonds, but it’s like comparing apples and oranges to compare bonds to stocks. Bonds are fixed income.

You can get burned on any asset of course… every investment has inherent risk – bonds too!

But junk bonds are well “junk”. Your comparison of some high yield stocks to junk bonds is not too far off.

Check out the links on the dangers of high yiled stocks – I specifically discuss the risks of that particular asset. These are different risks than REITs. 🙂

Cheers

Avrom

I am not trying to compare bonds with stocks. My point was what you already said, that you can get burned in any asset.

But I have very little knowledge about bonds. My only point was you can get trashed with high yields no matter what vehicle you are using.

Avrom, really good stuff in these dangers of high yield stock articles. I especially like the rules of thumb for yields that are too high and the dividend payout ratio amount. Many investors that are now reaching for yield should read these so they know the risks involved.

Ben, thanks! 😉

I do agree with your point, that dividend growth is more important than dividend yield. I sleep better at night with big blue-chip dividend growth companies.

However just to throw a wrench in the works, the ROI (return on investment) from my high yield small-cap stocks, which have virtually zero dividend growth, have outperformed the big blue chips. 🙂

This is why I firmly believe you need to diversify your stocks among more than one type of model. It doesn’t mean I blindly invest in any high yield stocks – it just means I have a level of diversification.

Cheers

Avrom

I agree. I am trying to take the average way approach – high current yield with as high growth as possible. I also take high yielders now, since I am reinvesting all dividends I collect. With that I also believe I can achieve better return.

Good points. The level of the yield is not as important as the consistency of the yield (in the payout and in the dividend increase). Most times an investment has a high yield for a reason and that is to compensate an investor for the risk they are taking in the investment.

Higher yields are not always a bad investment…the price you pay and the margin of safety matter more than anything, but it makes sense to realize your risks before making any investment.

Ben, I agree. Not an easy task. You can get sucked into the yield shinny glittering and later suffer loses.

I try to keep my evaluations as easy as possible, but sometimes evaluating your risk is very confusing. Too many variables.

Right, the hardest part about investing is the high amount of unknowns involved. Once investors are able to admit that there are so many factors that are out of their control, they can focus on the really important things like having a systematic process (to stay with through the ups and downs), keeping costs low, having a long-term point of view and keeping trading to a minimum.