The following is a guest post by Ben Carlson from A Wealth of Common Sense. If you would like to submit a guest post to The Dividend Ninja, check out our guest posting guidelines.

“Compare this with a 50% drawdown in stocks in the past bear market and you can see that bonds and stocks do not have the same characteristics for loss. Interest rates would really need to spike higher in a very short period of time to equal stock losses. And unfortunately, rates can stay low for long periods of time.”

Dividend Stocks are Not a Bond Substitute

With interest rates at generational lows, investors are in search of yield. The 10 Year U.S. Treasury is currently yielding around 1.7%. As late as 2006 the 10 Year yielded over 5.0% and in 2000 it was over 6.0%. By keeping short-term interest rates pegged at basically zero, the Fed is forcing investors to reach for yield and move out further on the risk spectrum.

With interest rates at generational lows, investors are in search of yield. The 10 Year U.S. Treasury is currently yielding around 1.7%. As late as 2006 the 10 Year yielded over 5.0% and in 2000 it was over 6.0%. By keeping short-term interest rates pegged at basically zero, the Fed is forcing investors to reach for yield and move out further on the risk spectrum.

Stocks have been a huge beneficiary of this interest rate policy. Since the lows in 2009, stock markets around the globe are up over 100% in many cases. Bonds have also performed well and now have lower interest rates to show for it. Because of the low rates many market experts are now saying the bond market is in a bubble that is bound to burst through rising interest rates (rates and prices are inversely related).

This interest rate environment has allowed corporations to issue debt at very low rates. Easy access to debt and a recovering economy has given corporations the luxury of being able to buy back their own shares and increase dividends after many had suspended or cut back on this shareholder friendly activity at the depths of the Great Recession. This has led many investors to look at stable, blue-chip dividend-producing stocks as alternative sources of yield in this low-interest rate environment.

Over time dividends are a great way to increase your income and possibly even reduce the volatility of your stock portfolio. But it would be a mistake to assume that dividends can act as a substitute for the bond portion of your portfolio. This is because the volatility and risk of large losses are still much greater with dividend producing stocks than with bonds.

Looking at Dividend ETFs

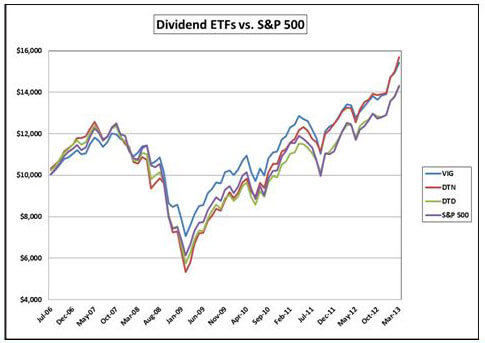

Let’s take a look at the historical performance of some dividend ETFs to see why you should not look at them as bond-like investments. WisdomTree has become known as a proponent of dividends based on their founder, Jeremy Siegel, and his research on dividend investments. The WisdomTree Total Dividend ETF (ticker DTD) tracks the company’s dividend index.

They also have the WisdomTree Dividends ex-Financials (ticker DTN) that is similar but doesn’t carry financial stocks which had artificially high dividend rates in the crash that were suspended in most cases. And Vanguard has the Dividend Appreciation ETF (ticker VIG) which tracks an index of stocks that have a history of increasing dividends consistently over time.

In the chart and graph below are some relevant statistics on these funds since their inception (all started in 2006) and also a graph that shows how a $10,000 investment in each of these ETFs has performed against the S&P 500 Index in that period of time.

You will notice that dividends helped all of these funds outperform the S&P 500 over this time frame. That makes sense since reinvested dividends play a larger role in your long-term performance than most investors assume. But if you look at the standard deviation and beta (correlated volatility to the S&P) numbers you will notice that the results look very similar to most stock funds.

The VIG has a lower beta and standard deviation of returns but the DTD and DTN aren’t much different and in fact, they have a higher standard deviation than the market. This means they were actually more volatile than the market since 2006. And the graph shows that dividends didn’t help too much with the drawdown in 2008 and 2009 either. The WisdomTree ETFs both lost over 50% of their value and the Vanguard ETF was down more than 40% from peak to trough.

Looking at Bond ETFs

Now let’s look at how much bonds can lose if interest rates rise in the future. The IEF ETF tracks the 7-10 year Treasury Bond Index and currently has a duration of 7.56. That means that for every 1.0% increase in interest rates the fund would be expected to lose a little over 7.5%. Netting out the current 1.6% yield would give you a total loss of just under 6.0%.

Compare this with a 50% drawdown in stocks in the past bear market and you can see that bonds and stocks do not have the same characteristics for loss. Interest rates would really need to spike higher in a very short period of time to equal stock losses. And unfortunately, rates can stay low for long periods of time.

Longer-dated bonds will have a higher duration so you could see larger losses in those securities when rates rise. On the other hand, shorter duration bonds will lose less once rates rise. So if dividends aren’t the answer to calm your bond nerves then what are the alternatives?

Reaching for yield usually does not end well for investors. That is one of the defining lessons of the subprime mortgage debacle. Higher reward always leads to higher risk. To increase your returns over treasury rates, money markets and CDs you could look to corporate bonds and emerging markets. The LQD ETF tracks the corporate bond market and currently yields about 3.6%. And EMB is an emerging markets bond ETF that yields 4.1%.

These still are not the 5-6% rates of the past but they still offer a nice spread over low-yielding treasuries market and near-zero money market funds. And they have similar duration numbers to the IEF so your interest rate risk is similar in these funds if rates rise. Fixed income is not where you should plan on taking on huge amounts of risk anyways since that is the portion of your portfolio that is used to reduce volatility and preserve your savings.

Conclusion – Not a Bond Substitute

It makes sense that dividend stocks can be used to increase your long-term investment performance but they should not be considered an alternative to bonds. They are not a bond substitute. It is also possible to decrease your volatility and increase the quality of your portfolio through dividend-paying stocks.

Make sure you understand the volatility and loss attributes before assuming that dividend stocks will be the answer to your bond worries and a bond substitute. You need to make sure you make an apples-to-apples comparison so you know all of the risks involved.

Did not understand or know the difference in volatility between dividend stocks and bonds and boy the risks are quite different. Thanks for the insight. So with interest rates so low what is a conservative investor to do other than not using dividend stocks as a substitute for bonds? Any investment suggestions?

Steven, bonds are still a good safety-net when markets go nuts. If we have a big sell-off this May or an unexpected crisis, you are going to need those bonds to cushion the blow. With stock markets hitting five-year highs that is quite a possibility.

The looming problem is rising interest rates. Bond prices will definitely decline when interst rates rise, no doubts about that. The question is when and how sharply will they rise? So far that doesn’t appear to be anytime soon.

For now I would keep my bonds, and if interest rates start to steadily rise then shift a portion of my fixed-income into MMKT Funds and GICs (CD’s). I’m not a professional financial advisor but that is what I am planning for my portfolio.

Cheers

Thanks fro the response. The interest rates are so puny now, there is not much to do. Maybe ladder out some CDs, although not sure that really matters too much.

I agree. The total return on bonds will be lower in a rising rate environment but you will still be able to receive your interest payments to offset some price losses. Rates can stay low for a very long time or rise very quickly so it’s hard to predict where they will go in the short-term.

A good strategy could be to ladder your bonds with short-term and intermediate-term holdings but stay away from longer dated bonds. The 20-30 year bonds will have the biggest losses with rising rates. Diversifying by maturity dates will allow you to have protection on the downside (short-term funds) and still get some yield (intermediate -term). Then if rates do rise you can slowly increase your maturity profile to earn a higher yield.

This is not an easy thing to plan for as we have had about 30 years of rates in decline.

Ben I agree. The majority of my bond holdings are in short-term bond ETFs such as iShares CLF. This is a 1-5 year laddered bond ETF of Canadian short-term govt. bonds.

Thanx for the post! 😉

Cheers

No one knows when interest rates will rise and by how much, so I can suggest what I have done and invite comments. ( I am in Canada btw, but everything suggested is available to US investors as well) For my bond portion ( 20%) I use CBO which is 1-5 yr laddered bonds, presently paying a 4.39% dividend. For my preferred shares portion ( 20%) I use XPF, which is North American preferred blue chip stocks, which pays a divvy of 5.02% I use a 10% of my portfolio for reits ( XRE) which pays 4.35% For dividend I have 20% in XEI which is an equity income etf paying 4.78% and another 20% in CVY which is a U.S. multi asset income fund paying 5.27% and 10% in cash. I am 59 and retired so I want income but prefer to balance my portfolio across blue chip, preferreds & bonds with exposure to both of our great countries.

Brian sounds good to me! I think we are going to need those bonds in 2014 – or even sooner. Just two points. 🙂

For the bond ETFs, you must look at YTM (Yield to Maturity) and not just the yield from the coupons. This is your true return on investment. Your principal for funds like CBO and CLF will likely decline somewhat over time.

I also like preferred shares. Also remember that PFs are tied into the longer bond durations. SO you could potentially get hit just as hard with PFs as bonds, in an increasing rate environment.

But I like your portfolio and approach. 😉

Cheers

What are your thoughts on diversifying the bond portion ( CBO) by replacing it with XTR which has a more income oriented approach?

Brian, you are right about the fact that no one knows when rates will rise. I like the fact that you have a very diversified income portfolio. Because when rates do rise not every income producing investment will react the same. Some will do better than others so it’s a good idea to stay diversified.

I looked at XTR and it looks to me to be very similar to your diversified portfolio since it has some high yield, dividend stocks, corporates and preferred stocks. It does have a higher yield than CBO but it will probably do worse if rates rise and it will have much more volatile price action.

You need to determine whether you would like the higher yield now or the rising rate protection in the future.

Preferred shares. 😉

Thanks Ninja & Ben for your insightful comments. I agree that when & if the rates rise there will be a short term negative effect on CBO, XTR & XPF as all bonds & preferreds will correct. They will reset at some point as some bonds in the etf mature and newer ones at the higher rate are purchased. As much as this is a “portfolio stabilizer” for me I am questioning myself if bonds & preferreds totalling 40% of the overall portfolio is justified in this present interest rate environment. Conversation & comments always welcome 🙂